Published on Jul 30, 2019

Updated on May 18, 2020

Create superior customer experiences to enhance competitive advantage.

Go from zero to breakthrough with scalable, future-proof solutions.

Harness deep tech for smarter solutions and maximum impact.

Accelerate value delivery with powerful pre-built digital tools.

Help businesses connect with an internet first generation.

Test the smarter way: where precision meets efficiency.

Unlock real-time and personalized customer journeys for mobile first generation.

Turn data into decisive action with scalable AI infrastructure.

Design agile digital foundations that scale with tomorrow's business needs.

Build new-age architecture for maximum efficiency and hyper-growth.

Fine-tune your cloud infrastructure for peak performance.

Automated compliance and control for global regulations.

All

Customer Experience

Mantra

Application Development

Insurtech

Digital Health

Insurance

Deep-Tech

AgriTech(1)

Augmented Reality(21)

Clean Tech(9)

Customer Journey(17)

Design(45)

Solar Industry(8)

User Experience(68)

Edtech(10)

Events(34)

HR Tech(3)

Interviews(10)

Life@mantra(11)

Logistics(6)

Manufacturing(5)

Strategy(18)

Testing(9)

Android(48)

Backend(32)

Dev Ops(11)

Enterprise Solution(33)

Technology Modernization(9)

Frontend(29)

iOS(43)

Javascript(15)

AI in Insurance(41)

Insurtech(67)

Product Innovation(59)

Solutions(22)

E-health(12)

HealthTech(25)

mHealth(5)

Telehealth Care(4)

Telemedicine(5)

Artificial Intelligence(154)

Bitcoin(8)

Blockchain(19)

Cognitive Computing(8)

Computer Vision(8)

Data Science(24)

FinTech(51)

Banking(7)

Intelligent Automation(27)

Machine Learning(48)

Natural Language Processing(14)

Microinsurance targets low-income households and individuals with little savings. Low premium, low caps, and low coverage limits are the characteristics of microinsurance plans. These are designed for risk-proofing the assets otherwise not served by traditional insurance schemes.

Because microinsurance comprises of low-premium models, it demands lower operational cost. This article covers insights on how AI can help bridge customer gaps for microinsurers.

Globally, microinsurance penetration is just around 2-3% of the potential market size. Following are the challenges that companies providing microinsurance policies face-

Fortunately, technology is capable of solving customer support, repetitive workflow, and scalability challenges to a great extent. The subsequent section measures the benefits of AI-based technology in the microinsurance sector.

Paperwork, handling numerous documents, data entry, etc. are current tedious tasks. AI-driven technologies like intelligent document processing systems can help simplify the insurance documentation and retrieval process.

For example, Gramcover, an Indian startup in the microinsurance sector uses direct-document uploading and processing for faster insurance distribution in the rural sector.

Because of scalability, technology has also enabled non-insurance companies to distribute insurance schemes on a disruptive scale.

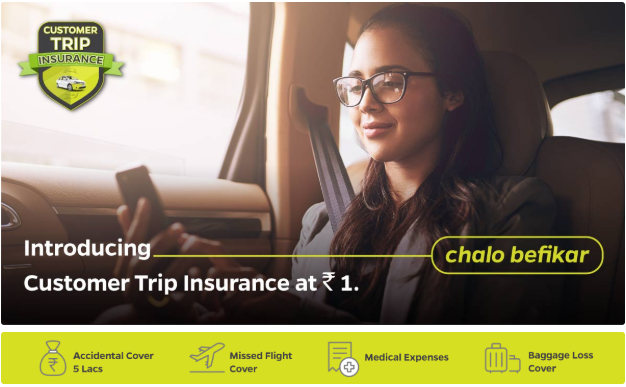

Within a year of launching the in-trip insurance initiative, cab-hailing service — Ola, is able to issue 2 crore in-trip policies per month. The policy offers risk coverage against baggage loss, financial emergencies, medical expenses, and missed flights due to driver cancellations/ uncontrollable delays.

AI-based systems are also cost-effective in the long run because the same system is adaptable across different platforms and is easily integrated across the enterprise.

The microinsurance space is in need of better customer-first policies that are both convenient and flexible to use. ‘On & Off’ microinsurance policies for farmers, especially when they need it, can bring about a change in their buying behavior. The freedom to turn your insurance protection off, when you are not likely to use or benefit from it can give customers the freedom to use a product that maximizes their utility.

At the same time, insurers will be able to diffuse their products with greater spread across the rural landscape because the customer is able to derive greater value from it.

Consumers want faster reimbursements against their plans. Going with the traditional process, claim settlement may take several months to approve. Through distributed ledgers and guided access, documents or information can be made available in a fraction of seconds.

MaxBupa, in association with Mobikwik, has introduced HospiCash, a microinsurance policy in the health domain. It has identified the low-income segment’s needs and accordingly takes cares of out of pocket expenses (@ ₹500/day) of the customers.

Mobikwik wallet ensures hassle-free everyday money credit to the user.

Another example of easy claim settlement is that of ICICI Lombard motor insurance e-claim service. InstaSpect, a live video inspection feature on the Lombard’s Insure app allows registering claim instantly and helps in getting immediate approvals. It also connects the user to the claim settlement manager for inspecting the damaged vehicle over a video call.

Real-time inspection and claims can benefit farmers. In the event of machine or tractor breakdown, they need not wait for days for the claim inspector to come in-person and assess the vehicle. Instead, using Artificial Intelligence and Machine Learning models, the inspection can be carried out within seconds via an app, following which the algorithm can determine (based on trained models) to approve or reject the claim.

Entering data manually is subject to human error, whereas, data entered through scanners, document parsers, etc. are up to 99.94% accurate.

Microinsurance sector is also a victim of self-centered human behavior, where agents consider personal profit before the benefit of the user. Automating the customer/agent onboarding journey can improve the distributed sales network model too.

MaxBupa uses FlowMagic for processing inbound documents, for enterprise-wide flexibility and fit. With AI, they are able to halve the manned human effort for gains in operational accuracy.

Automation can bring down the challenges of mis-selling, moral hazard, and distribution costs to level zero with agnostic digital systems.

Where human employment calls for dedicated working hours, with chatbots, a large number of queries can be handled anytime during the day, weekends, and holidays. It is even convenient for customers also.

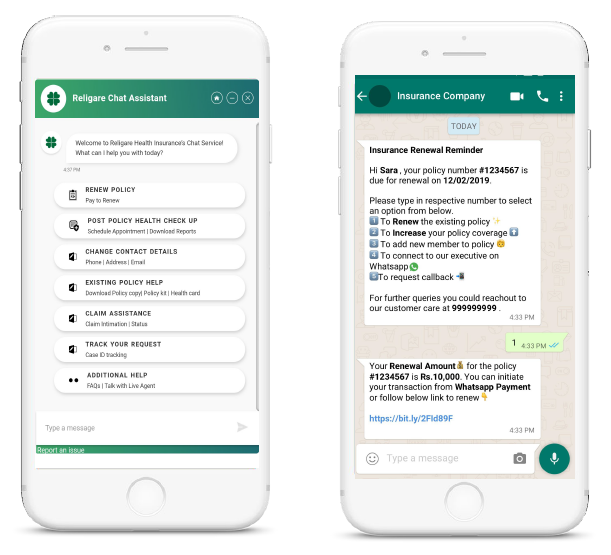

Religare, India’s leading insurance provider has introduced AI-based chatbots that can handle customer queries without needing human intervention. It is capable of helping a customer to buy or renew a policy, schedule appointments, updating contact details, and more. This technology has helped Religare to increase sales by 5X and increase customer interaction by 10X.

The microinsurance sector can also take advantage of chatbot technology to improve response time.

As more microinsurance products continue to surface in the market, insurers need to place the rural customer upfront and center of their strategic efforts. By understanding and fulfilling the rural insuree’s needs, cutting down operational costs through process automation such as adding AI-powered chatbots to handle general queries or quickly settling claims without the need for unnecessary human intervention — microinsurers can realize better market penetration and adoption for these policies.

Knowledge thats worth delivered in your inbox

Smart Manufacturing starts with real-time visibility.

Manufacturing companies today generate data by the second through sensors, machines, ERP systems, and MES platforms. But without real-time insights, even the most advanced production lines are essentially flying blind.

Manufacturers are implementing real-time dashboards that serve as control towers for their daily operations, enabling them to shift from reactive to proactive decision-making. These tools are essential to the evolution of Smart Manufacturing, where connected systems, automation, and intelligent analytics come together to drive measurable impact.

Data is available, but what’s missing is timely action.

For many plant leaders and COOs, one challenge persists: operational data is dispersed throughout systems, delayed, or hidden in spreadsheets. And this delay turns into a liability.

Real-time dashboards help uncover critical answers:

By converting raw inputs into real-time manufacturing analytics, dashboards make operational intelligence accessible to operators, supervisors, and leadership alike, enabling teams to anticipate problems rather than react to them.

Line performance and downtime trends

Track OEE in real time and identify underperforming lines.

Predictive maintenance alerts

Utilize historical and sensor data to identify potential part failures in advance.

Inventory heat maps & reorder thresholds

Anticipate stockouts or overstocks based on dynamic reorder points.

Quality metrics linked to operator actions

Isolate shifts or procedures correlated with spikes in defects or rework.

These insights allow production teams to drive day-to-day operations in line with Smart Manufacturing principles.

Role-based dashboards

Dashboards can be configured for machine operators, shift supervisors, and plant managers, each with a tailored view of KPIs.

Embedded alerts and nudges

Real-time prompts, like “Line 4 below efficiency threshold for 15+ minutes,” reduce response times and minimize disruptions.

Cross-functional drill-downs

Teams can identify root causes more quickly because users can move from plant-wide overviews to detailed machine-level data in seconds.

Data lakehouse integration

Unified access to ERP, MES, IoT sensor, and QA systems—ensuring reliable and timely manufacturing analytics.

ETL pipelines

Real-time data ingestion from high-frequency sources with minimal latency.

Visualization tools

Custom builds using Power BI, or customized solutions designed for frontline usability and operational impact.

Mantra Labs partnered with a North American die-casting manufacturer to unify its operational data into a real-time dashboard. Fragmented data, manual reporting, delayed pricing decisions, and inconsistent data quality hindered operational efficiency and strategic decision-making.

As this case shows, real-time dashboards are not just operational tools—they’re strategic enablers.

(Learn More: Powering the Future of Metal Manufacturing with Data Engineering)

| Aspect | What You Should Know |

| 1. Why Static Reports Fall Short | Delayed insights after issues occur Disconnected systems (ERP, MES, sensors) No real-time alerts or embedded decision logic |

| 2. What Real-Time Dashboards Enable | Track OEE and downtime in real-time Predictive maintenance using sensor data Dynamic inventory heat maps Quality linked to operators |

| 3. Dashboards That Drive Action | Role-based views (operator to CEO) Embedded alerts like “Line 4 down for 15+ mins” Drilldowns from plant-level to machine-level |

| 4. What Powers These Dashboards | Unified Data Lakehouse (ERP + IoT + MES) Real-time ETL pipelines Power BI or custom dashboards built for frontline usability |

Smart Manufacturing dashboards aren’t just analytics tools—they’re productivity engines. Dashboards that deliver real-time insight empower frontline teams to make faster, better decisions—whether it’s adjusting production schedules, triggering preventive maintenance, or responding to inventory fluctuations.

Explore how Mantra Labs can help you unlock operations intelligence that’s actually usable.

Knowledge thats worth delivered in your inbox

Our Sales Team will be in touch with you shortly.

Hello Stranger! Please fill in a few details,and you’ll receive a link to this case study.

We have mailed you this case study.

We have mailed you this case study.

Thanks for subscribing.