3 minutes, 47 seconds. read

Published on Feb 21, 2019

Updated on Dec 2, 2019

Create superior customer experiences to enhance competitive advantage.

Go from zero to breakthrough with scalable, future-proof solutions.

Harness deep tech for smarter solutions and maximum impact.

Accelerate value delivery with powerful pre-built digital tools.

Help businesses connect with an internet first generation.

Test the smarter way: where precision meets efficiency.

Unlock real-time and personalized customer journeys for mobile first generation.

Turn data into decisive action with scalable AI infrastructure.

Design agile digital foundations that scale with tomorrow's business needs.

Build new-age architecture for maximum efficiency and hyper-growth.

Fine-tune your cloud infrastructure for peak performance.

Automated compliance and control for global regulations.

All

Customer Experience

Mantra

Application Development

Insurtech

Digital Health

Insurance

Deep-Tech

AgriTech(1)

Augmented Reality(21)

Clean Tech(9)

Customer Journey(17)

Design(45)

Solar Industry(8)

User Experience(68)

Edtech(10)

Events(34)

HR Tech(3)

Interviews(10)

Life@mantra(11)

Logistics(6)

Manufacturing(5)

Strategy(18)

Testing(9)

Android(48)

Backend(32)

Dev Ops(11)

Enterprise Solution(33)

Technology Modernization(9)

Frontend(29)

iOS(43)

Javascript(15)

AI in Insurance(41)

Insurtech(67)

Product Innovation(59)

Solutions(22)

E-health(12)

HealthTech(25)

mHealth(5)

Telehealth Care(4)

Telemedicine(5)

Artificial Intelligence(154)

Bitcoin(8)

Blockchain(19)

Cognitive Computing(8)

Computer Vision(8)

Data Science(24)

FinTech(51)

Banking(7)

Intelligent Automation(27)

Machine Learning(48)

Natural Language Processing(14)

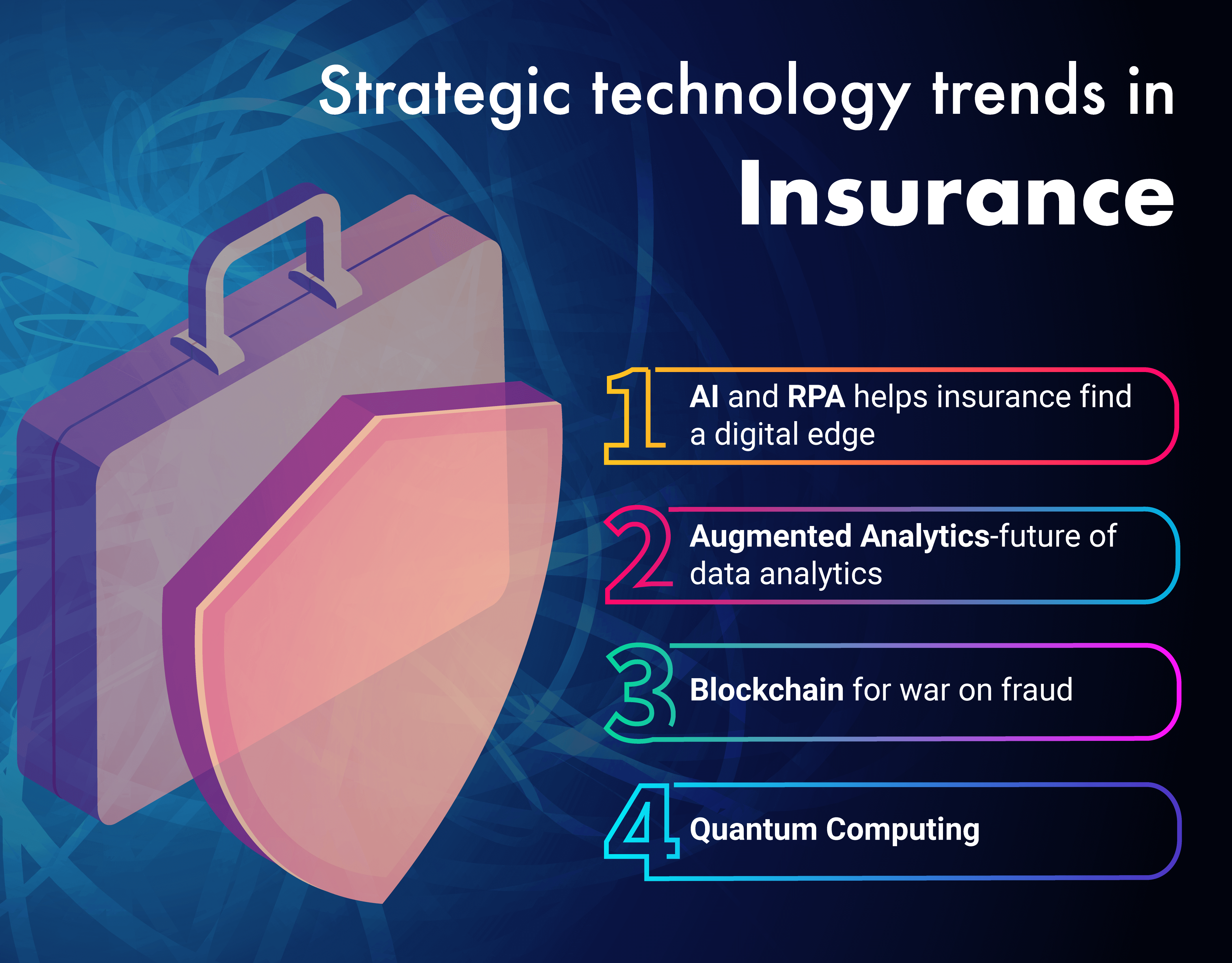

“Strategic technology trend is one with substantial disruptive potential, that is beginning to break out of an emerging state into broader impact and use, or which are rapidly growing trends with a high degree of volatility reaching tipping points over the next five years”, says Gartner.

These technology trends shall enable insurers to expand into more ecosystems than ever before. Let us explore such strategic technology trends, which will impact the insurers in the near future.

1. AI & RPA helps insurance find a digital edge:

AI and RPA are already a reality for insurance. AI has found its way into vehicles, homes, and businesses and in the Insurance industry as well, it solves the necessary day-to-day tasks of running a business by the automation of routine patterns. It is able to tailor solutions for individual customers and replace the one-size-fits-all products currently available. “AI in insurance will allow carriers to deliver scalable and customized solutions for members and policyholders,” says Ramon Lopez, Vice President of Property & Casualty Claims and Innovation at USAA.

RPA tools currently occupy the Peak of Inflated Expectations in the Gartner Hype Cycle for Artificial Intelligence, 2018. RPA is widely adopted in various industries, insurance included. “End-user organizations adopt RPA technology as a quick and easy fix to automate manual tasks,” said Cathy Tornbohm, vice president at Gartner. In the insurance industry automation of the day-to-day tasks would potentially reduce cost, time consumption and increase accuracy, quality and competency.

2. Augmented Analytics- future of data analytics:

One of the latest advancements for business development tools is the advent of augmented analytics. As per a report from Deloitte “Augmented analytics marks the next wave of disruption in the data analytics market”. It is an approach that automates insights using machine learning and natural language generation. Gartner predicts “by 2020, more than 40% of data science tasks will be automated”, resulting in increased productivity and broader use by data scientists. According to Accenture, “1 out of 3 insurers globally now uses Big Data from IoT technologies, such as Fitbit, Samsung Gear or Apple watch to collect lifestyle data from insureds”. Augmented Analytics will help reap business value from those data by automating Big Data insights. The insurance industry is expected to be the biggest beneficiary as it will help increase the accuracy and end the traditional “gut-feeling” decision-making approach.

3. Blockchain for war on fraud:

Blockchain is one of the biggest fourth industrial revolutions for many industries, including insurance. Insurance fraud costs more than $40 billion a year. The insurance companies can use “the distributed ledger” to potentially lower fraudulent claims, cost, transaction settlement time and improve cash flow.EY, Guardtime, A.P. Møller-Maersk, Microsoft, and ACORD collaborated and launched blockchain-powered marine hull insurance platform Insurwave in 2018. The platform is now in commercial use and handled risk for more than 1,000 commercial vessels and 500,000 automated transactions in its first twelve months of operation. More than 38 insurance companies have embarked on an initiative called the B3i to explore Blockchain applications in insurance. “In the past decade, technological advances from artificial intelligence to Blockchain have transformed business models in every sector and insurance is no exception. Dubai World Insurance Congress embraced the future of the industry with insights from the sector’s most established and innovative leaders,” said Arif Amiri, Chief Executive Officer of DIFC Authority.

International Data Corporation (IDC) analysis shows “worldwide spending on Blockchain solutions could reach $11.7 Bn in 2022”. Blockchain gives the insurance company an independently verifiable data set so they don’t have to rely on the customer’s version. It is emerging as the central repository of truth for many blockchain use-cases. According to Gartner reports, “Blockchain will create $3.1T in business value by 2030”.

4. Quantum Computing:

Quantum computing is rising on the Gartner Hype Cycle. It is expected to become one of the greatest disruptions of the age. Quantum computing has the ability to process huge datasets and models that would have previously taken days and weeks. It can help calculate risks, of almost any nature, such as the impact of an approaching hurricane on a specific region.

According to a recent Novarica executive report, “Quantum Computing and Insurance: Overview and Potential Players,” by Mitch Wein and Tom Kramer offer various use cases of quantum computing. However, not many insurers are working with quantum algorithms. They are still seen as technologies that are on the distant horizon and not in their face like artificial intelligence.

The insurance industry has a complex infrastructure and legal restrictions. However, with investments in these Strategic Technology trends, insurers can become more customer-centric, achieve growth and lower cost.

https://www.linkedin.com/pulse/case-study-insurance-industry-denis-mwarania

https://tractable.ai/blog/together-towards-ai-notes-from-insuretech-connect-2017

https://www.dig-in.com/list/top-5-insurance-quantum-computing-use-cases

https://www.cbinsights.com/research/blockchain-insurance-disruption/

Knowledge thats worth delivered in your inbox

Smart Manufacturing starts with real-time visibility.

Manufacturing companies today generate data by the second through sensors, machines, ERP systems, and MES platforms. But without real-time insights, even the most advanced production lines are essentially flying blind.

Manufacturers are implementing real-time dashboards that serve as control towers for their daily operations, enabling them to shift from reactive to proactive decision-making. These tools are essential to the evolution of Smart Manufacturing, where connected systems, automation, and intelligent analytics come together to drive measurable impact.

Data is available, but what’s missing is timely action.

For many plant leaders and COOs, one challenge persists: operational data is dispersed throughout systems, delayed, or hidden in spreadsheets. And this delay turns into a liability.

Real-time dashboards help uncover critical answers:

By converting raw inputs into real-time manufacturing analytics, dashboards make operational intelligence accessible to operators, supervisors, and leadership alike, enabling teams to anticipate problems rather than react to them.

Line performance and downtime trends

Track OEE in real time and identify underperforming lines.

Predictive maintenance alerts

Utilize historical and sensor data to identify potential part failures in advance.

Inventory heat maps & reorder thresholds

Anticipate stockouts or overstocks based on dynamic reorder points.

Quality metrics linked to operator actions

Isolate shifts or procedures correlated with spikes in defects or rework.

These insights allow production teams to drive day-to-day operations in line with Smart Manufacturing principles.

Role-based dashboards

Dashboards can be configured for machine operators, shift supervisors, and plant managers, each with a tailored view of KPIs.

Embedded alerts and nudges

Real-time prompts, like “Line 4 below efficiency threshold for 15+ minutes,” reduce response times and minimize disruptions.

Cross-functional drill-downs

Teams can identify root causes more quickly because users can move from plant-wide overviews to detailed machine-level data in seconds.

Data lakehouse integration

Unified access to ERP, MES, IoT sensor, and QA systems—ensuring reliable and timely manufacturing analytics.

ETL pipelines

Real-time data ingestion from high-frequency sources with minimal latency.

Visualization tools

Custom builds using Power BI, or customized solutions designed for frontline usability and operational impact.

Mantra Labs partnered with a North American die-casting manufacturer to unify its operational data into a real-time dashboard. Fragmented data, manual reporting, delayed pricing decisions, and inconsistent data quality hindered operational efficiency and strategic decision-making.

As this case shows, real-time dashboards are not just operational tools—they’re strategic enablers.

(Learn More: Powering the Future of Metal Manufacturing with Data Engineering)

| Aspect | What You Should Know |

| 1. Why Static Reports Fall Short | Delayed insights after issues occur Disconnected systems (ERP, MES, sensors) No real-time alerts or embedded decision logic |

| 2. What Real-Time Dashboards Enable | Track OEE and downtime in real-time Predictive maintenance using sensor data Dynamic inventory heat maps Quality linked to operators |

| 3. Dashboards That Drive Action | Role-based views (operator to CEO) Embedded alerts like “Line 4 down for 15+ mins” Drilldowns from plant-level to machine-level |

| 4. What Powers These Dashboards | Unified Data Lakehouse (ERP + IoT + MES) Real-time ETL pipelines Power BI or custom dashboards built for frontline usability |

Smart Manufacturing dashboards aren’t just analytics tools—they’re productivity engines. Dashboards that deliver real-time insight empower frontline teams to make faster, better decisions—whether it’s adjusting production schedules, triggering preventive maintenance, or responding to inventory fluctuations.

Explore how Mantra Labs can help you unlock operations intelligence that’s actually usable.

Knowledge thats worth delivered in your inbox

Our Sales Team will be in touch with you shortly.

Hello Stranger! Please fill in a few details,and you’ll receive a link to this case study.

We have mailed you this case study.

We have mailed you this case study.

Thanks for subscribing.