5 minutes, 5 seconds read

Published on Dec 16, 2019

Updated on May 11, 2020

Create superior customer experiences to enhance competitive advantage.

Go from zero to breakthrough with scalable, future-proof solutions.

Harness deep tech for smarter solutions and maximum impact.

Accelerate value delivery with powerful pre-built digital tools.

Help businesses connect with an internet first generation.

Test the smarter way: where precision meets efficiency.

Unlock real-time and personalized customer journeys for mobile first generation.

Turn data into decisive action with scalable AI infrastructure.

Design agile digital foundations that scale with tomorrow's business needs.

Build new-age architecture for maximum efficiency and hyper-growth.

Fine-tune your cloud infrastructure for peak performance.

Automated compliance and control for global regulations.

All

Customer Experience

Mantra

Application Development

Insurtech

Digital Health

Insurance

Deep-Tech

AgriTech(1)

Augmented Reality(21)

Clean Tech(9)

Customer Journey(17)

Design(45)

Solar Industry(8)

User Experience(68)

Edtech(10)

Events(34)

HR Tech(3)

Interviews(10)

Life@mantra(11)

Logistics(6)

Manufacturing(5)

Strategy(18)

Testing(9)

Android(48)

Backend(32)

Dev Ops(11)

Enterprise Solution(33)

Technology Modernization(9)

Frontend(29)

iOS(43)

Javascript(15)

AI in Insurance(41)

Insurtech(67)

Product Innovation(59)

Solutions(22)

E-health(12)

HealthTech(25)

mHealth(5)

Telehealth Care(4)

Telemedicine(5)

Artificial Intelligence(154)

Bitcoin(8)

Blockchain(19)

Cognitive Computing(8)

Computer Vision(8)

Data Science(24)

FinTech(51)

Banking(7)

Intelligent Automation(27)

Machine Learning(48)

Natural Language Processing(14)

The year 2019 has been a benchmark in insurance innovations that brought in new value propositions to the industry. What’s more remarkable is — both traditional Insurers and Insurtechs are striving to offer simple, convenient, and value-added customer-centric products coupled with technology initiatives. Here are 10 noteworthy insurance innovations that shaped the industry this year.

According to a recent EFMA-Accenture report, the insurance industry has witnessed growth in digital sales & services, Artificial Intelligence trends — especially machine learning and natural language processing (nlp), big data and analytics, cloud, intelligent automation, and blockchain.

However, insurance players are not just adding convenience through technology but also understanding the ‘actual’ customer needs and developing the products accordingly. Let’s discuss the impactful insurance innovations with their use cases in detail.

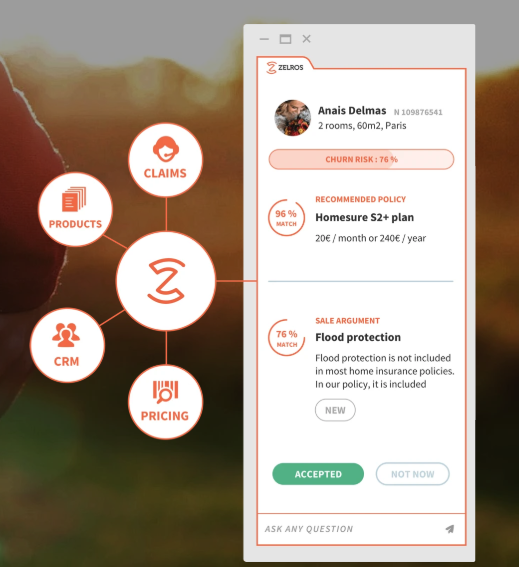

While most insurers are leveraging AI to understand customers and their requirements; another idea that hits the list is to complement the knowledge of insurance employees during sales pitches and customer services.

For example, Zelros is Augmenting intelligence of sales and customer representatives through real-time best product recommendations, advisory, and pricing based on studying the customer profile.

Similarly, Nippon Life Insurance Company has introduced an AI-powered TASKALL tablet for its sales representatives. This tablet identifies suitable prospects from the set of entire salesforce activities, thus enhancing the sales and customer representatives’ services.

Smart automation corresponds to deploying intelligent technologies to gain massive operational efficiency and at the same time create value for the end customer.

For example, South Korean Kyobo Life Insurance Co. Ltd. has developed an AI system BARO (Best Analysis & Rapid Outcome) to automate underwriting. The system uses NLP to allow sales and customer interactions in natural language.

In the same way, Religare incorporated AI-based chatbot in their workflow. Through this bot, the company has automated a number of operations like customer query resolution, customer engagement, and lead and ticket management.

Join our Webinar — AI for Data-driven Insurers: Challenges, Opportunities & the Way Forward hosted by our CEO, Parag Sharma as he addresses Insurance business leaders and decision-makers on April 14, 2020.

In 2018, in the US alone, nearly 1.2 million people worked for insurance agencies, brokers, and insurance-related enterprises. This indicates the prominence of the brokerage in insurance. Brokers might not be directly involved in product development, risk evaluation, etc.; but they play a pivotal role in insurance distribution.

For example, Gramcover, an Indian composite insurance broking firm is leveraging mobile technologies to minimize the inefficiencies and transaction costs in distributing micro-policies.

Also read – The case for a digital brokerage

The year 2019 also witnessed the entry of technology giants like Alibaba entering the insurance space, and people welcoming them made the competition even more fierce. The World Insurtech Report 2019 states that nearly 30% of customers are interested in buying at least one insurance product from BigTech firms like Google, Apple, Facebook, Amazon, and Alibaba.

Insurers have thus realized to embrace the ecosystem-based digital economy to deliver richer customer experiences. AG Insurance’s Phil at Home is an example of ‘beyond’ insurance services to support customers in their day to day life. The app provides house maintenance services like plumbing, electricity, etc. along with medication reminders, food delivery, etc. to its elderly customers.

Also read – The Belgian Insurance Landscape

Blockchain or distributed ledger technology (DLT) brings transparency to a range of insurance processes along with the secure sharing of information. The innovative use of blockchain in insurance is to reduce redundant efforts.

For example, the US-based Aon Benfield along with partners have developed a blockchain-powered reinsurance placement solution to bring brokers and reinsurers on a collaborative platform.

Similarly, the Hong Kong Federation of Insurers in collaboration with CryptoBLK developed MIDAS (Motor Insurance DLT-based Authentication System) to authenticate motor insurance policy documents across the network in real-time.

Insurers’ partnerships with Insurtechs, Fintechs, and external players are presenting an opportunity to explore new customer base, test different business models, and get access to new technology frontiers.

For example, AXA partnered with ContGuard, which provides real-time cargo tracking services. Their product — Connected Cargo Solution gives customers 24/7 monitoring and data to AXA’s risk engineers to develop loss prevention plans. This also helps underwriters to quote the price with increased accuracy.

Addressing the customers’ demand for personalized services, Insurers have started applying AI to understand their sentiments and requirements. They have realized that real-time digital services unlock values for both carriers and customers.

For example, the UK-based Bought By Many helps people find insurance for uncommon assets like pets, shoes, gadgets, etc. The company also negotiates with insurers for the best deals.

The World Insurtech report 2019 reveals that nearly 41% of customers are ready to consider usage-based insurance and 37% want to explore on-demand insurance coverage. While usage-based insurance models provide as-you-go premium coverage based on customer’s potential for risky behavior; on-demand insurance allows customers to get cost-effective and convenient coverage depending on their needs.

For example, The Dinghy is an app-based on-demand freelancer insurer. It is also the world’s first on-demand professional indemnity insurance covering public liability, business equipment, legal expenses, and cyber liability.

Insurers are deploying machine learning models for risk assessment and mitigation. It not only makes the underwriting more accurate but also boosts profits by diminishing risks.

For example, ZestFinance uses automated machine learning tools to correlate current and traditional data. It helps to effectively gauge risks and outreach potential new customers.

Pricing still presents a bigger competitive advantage than many other insurance features. Accenture’s 2019 Global Financial Services Consumer Study states – more than 75% of customers can share their personal information for better prices.

Therefore, educating customers about potential risks isn’t sufficient. Coupling this information with available products’ prices and benefits is a must. For example, Jerry, a California-based personal insurance marketplace checks if the user is paying the best price for the insurance services. Based on an initial questionnaire, their AI-powered tools takes roughly 45 seconds to compare quotes from leading insurers and suggest optimum rate to the user.

Also read “Top 5 smartest AI-powered machines on earth.”

Knowledge thats worth delivered in your inbox

Smart Manufacturing starts with real-time visibility.

Manufacturing companies today generate data by the second through sensors, machines, ERP systems, and MES platforms. But without real-time insights, even the most advanced production lines are essentially flying blind.

Manufacturers are implementing real-time dashboards that serve as control towers for their daily operations, enabling them to shift from reactive to proactive decision-making. These tools are essential to the evolution of Smart Manufacturing, where connected systems, automation, and intelligent analytics come together to drive measurable impact.

Data is available, but what’s missing is timely action.

For many plant leaders and COOs, one challenge persists: operational data is dispersed throughout systems, delayed, or hidden in spreadsheets. And this delay turns into a liability.

Real-time dashboards help uncover critical answers:

By converting raw inputs into real-time manufacturing analytics, dashboards make operational intelligence accessible to operators, supervisors, and leadership alike, enabling teams to anticipate problems rather than react to them.

Line performance and downtime trends

Track OEE in real time and identify underperforming lines.

Predictive maintenance alerts

Utilize historical and sensor data to identify potential part failures in advance.

Inventory heat maps & reorder thresholds

Anticipate stockouts or overstocks based on dynamic reorder points.

Quality metrics linked to operator actions

Isolate shifts or procedures correlated with spikes in defects or rework.

These insights allow production teams to drive day-to-day operations in line with Smart Manufacturing principles.

Role-based dashboards

Dashboards can be configured for machine operators, shift supervisors, and plant managers, each with a tailored view of KPIs.

Embedded alerts and nudges

Real-time prompts, like “Line 4 below efficiency threshold for 15+ minutes,” reduce response times and minimize disruptions.

Cross-functional drill-downs

Teams can identify root causes more quickly because users can move from plant-wide overviews to detailed machine-level data in seconds.

Data lakehouse integration

Unified access to ERP, MES, IoT sensor, and QA systems—ensuring reliable and timely manufacturing analytics.

ETL pipelines

Real-time data ingestion from high-frequency sources with minimal latency.

Visualization tools

Custom builds using Power BI, or customized solutions designed for frontline usability and operational impact.

Mantra Labs partnered with a North American die-casting manufacturer to unify its operational data into a real-time dashboard. Fragmented data, manual reporting, delayed pricing decisions, and inconsistent data quality hindered operational efficiency and strategic decision-making.

As this case shows, real-time dashboards are not just operational tools—they’re strategic enablers.

(Learn More: Powering the Future of Metal Manufacturing with Data Engineering)

| Aspect | What You Should Know |

| 1. Why Static Reports Fall Short | Delayed insights after issues occur Disconnected systems (ERP, MES, sensors) No real-time alerts or embedded decision logic |

| 2. What Real-Time Dashboards Enable | Track OEE and downtime in real-time Predictive maintenance using sensor data Dynamic inventory heat maps Quality linked to operators |

| 3. Dashboards That Drive Action | Role-based views (operator to CEO) Embedded alerts like “Line 4 down for 15+ mins” Drilldowns from plant-level to machine-level |

| 4. What Powers These Dashboards | Unified Data Lakehouse (ERP + IoT + MES) Real-time ETL pipelines Power BI or custom dashboards built for frontline usability |

Smart Manufacturing dashboards aren’t just analytics tools—they’re productivity engines. Dashboards that deliver real-time insight empower frontline teams to make faster, better decisions—whether it’s adjusting production schedules, triggering preventive maintenance, or responding to inventory fluctuations.

Explore how Mantra Labs can help you unlock operations intelligence that’s actually usable.

Knowledge thats worth delivered in your inbox

Our Sales Team will be in touch with you shortly.

Hello Stranger! Please fill in a few details,and you’ll receive a link to this case study.

We have mailed you this case study.

We have mailed you this case study.

Thanks for subscribing.