Published on Sep 25, 2019

Updated on Nov 6, 2019

Create superior customer experiences to enhance competitive advantage.

Go from zero to breakthrough with scalable, future-proof solutions.

Harness deep tech for smarter solutions and maximum impact.

Accelerate value delivery with powerful pre-built digital tools.

Help businesses connect with an internet first generation.

Test the smarter way: where precision meets efficiency.

Unlock real-time and personalized customer journeys for mobile first generation.

Turn data into decisive action with scalable AI infrastructure.

Design agile digital foundations that scale with tomorrow's business needs.

Build new-age architecture for maximum efficiency and hyper-growth.

Fine-tune your cloud infrastructure for peak performance.

Automated compliance and control for global regulations.

All

Customer Experience

Mantra

Application Development

Insurtech

Digital Health

Insurance

Deep-Tech

AgriTech(1)

Augmented Reality(21)

Clean Tech(9)

Customer Journey(17)

Design(45)

Solar Industry(8)

User Experience(68)

Edtech(10)

Events(34)

HR Tech(3)

Interviews(10)

Life@mantra(11)

Logistics(6)

Manufacturing(5)

Strategy(18)

Testing(9)

Android(48)

Backend(32)

Dev Ops(11)

Enterprise Solution(33)

Technology Modernization(9)

Frontend(29)

iOS(43)

Javascript(15)

AI in Insurance(41)

Insurtech(67)

Product Innovation(59)

Solutions(22)

E-health(12)

HealthTech(25)

mHealth(5)

Telehealth Care(4)

Telemedicine(5)

Artificial Intelligence(154)

Bitcoin(8)

Blockchain(19)

Cognitive Computing(8)

Computer Vision(8)

Data Science(24)

FinTech(51)

Banking(7)

Intelligent Automation(27)

Machine Learning(48)

Natural Language Processing(14)

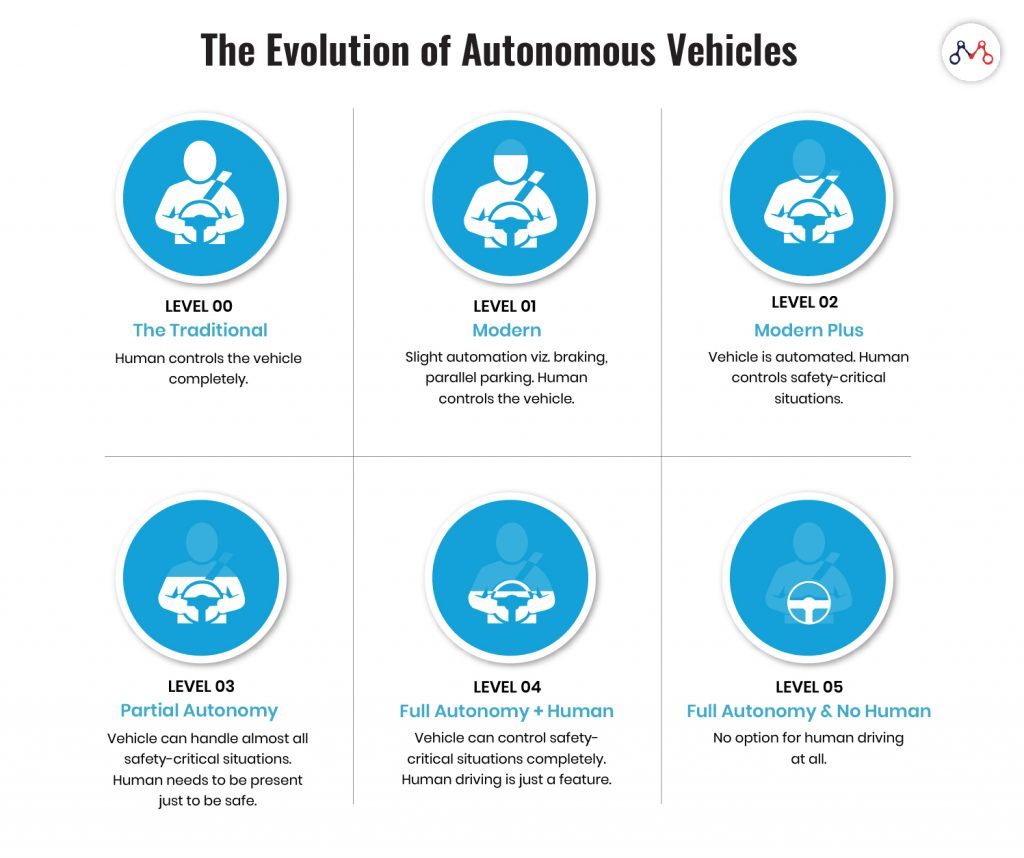

We’re about to witness the evolution of autonomous vehicles from Level 0 to Level 2. While Level 0 is completely human-driven; Level 1 vehicles can control braking and parallel parking themselves. Level 2 vehicles can operate automatically, but with a human ready to control exceptional situations.

The success of self-driving cars depends solely on the safety it brings to transportation. With increased safety, will we even need insurance for autonomous vehicles?

Perhaps, the traditional insurance policies might face a setback. But, autonomous vehicles will certainly open new avenues for innovative insurance products.

The Stevens Institute of Technology predicts that there would be over 23 million fully autonomous vehicles by 2035 in the US alone.

To stay competitive with the changing dynamics of auto insurance, insurers need to address new risks. But before, let’s take a look at potential risks in the autonomous vehicle insurance sector.

The shift to autonomous vehicles tends to bring dramatic changes in auto insurance premiums.

Instead of individual policies, researchers foresee insurance policies turning towards original equipment manufacturers (OEMs) and service providers such as ride-sharing companies. The new auto insurance products would be an outcome of the following transportation changes.

With autonomous vehicles on the roads, safety regulations are prone to change. For instance, the US National Highway Traffic Safety Administration intends to reconsider its current safety standards to accommodate AVs in existing transportation. But, this reformation will take the presence of human drivers into account.

With increased safety and reduced accident claims, the revenues from traditional premium policies might decline.

Insurers often follow a “no-fault” system to lower auto insurance costs by taking small claims out of the courts. For minor injuries, insurers compensate their policyholders regardless of who was at fault in the accident.

However, fender-benders would be more than it is with autonomous vehicles. Also, blockchain in insurance would become integral to investigate the root cause of the accident. And, of course, there won’t be much scope for lenient “no-fault” policies.

Traditional liability insurance pays for the policyholder’s legal responsibility to others for bodily injury or property damage. With autonomous vehicles, the liability is going to shift towards OEMs, suppliers, or car-rental service providers.

Currently, automakers must adhere to around 75 safety standards. This underwriting considers that a licensed driver will control the vehicle. The safety standards are going to change with more AVs on roads.

The present-day premium is high for a handful of autonomous vehicles because of insufficient data with underwriters and actuaries. However, chances are, major OEMs will cover the insurance premiums in the vehicle cost.

For instance, Tesla, one of the pioneers of autonomous vehicles, provides auto insurance at 30% lower rates than other insurance providers. Tesla having a better understanding of its vehicles’ technology and repair costs, believes can provide low-cost insurance. This is also a threat to insurance carrier fees.

Accenture estimates that autonomous vehicles will generate at least $81 billion in new insurance revenues in the US between 2020 and 2025. It also foresees opportunities for insurers in cybersecurity, product, and infrastructure landscapes. Let’s take a look at new auto insurance avenues.

While AVs ensure safety, there are unidentified cybersecurity threats. Vehicles fueled by IoT technology deal with comprehensive telematics data. Capturing every moment of the user proposes risks like identity theft, privacy invasion, misuse of personal information, and attacks from ransomware. According to the Center for Strategic and International Studies and McAfee, globally cybercrimes cost around $600 billion annually. The shared data from autonomous vehicles bring the financial sector at risk.

On the other hand, monitoring the performance of vehicles and the driver’s behavior behind the wheel can reduce claim investigation turn around time.

Therefore, future insurance products will also focus on moral and financial threats to passengers.

The product liability insurance might shift from automotive to sensors and algorithms behind the autonomous vehicle. The OEMs will be also liable for communication or Internet connection failure along with machinery and software failures.

It will take more than 30 years for autonomous vehicles to completely dominate transportation. The upcoming insurance products will take existing infrastructure into account. For example, AVs need insurance if it damages due to puddles or potholes on the road.

Also, car ownership tends to decline with rental and pay-as-you-use models. This opens a fleet-level opportunity for insurers for driverless cars.

Source: Accenture X Stevens Institute of Technology “Insuring Autonomous Vehicles” report

Insurers need to adapt to the rapid technological advancements. Cloud-based insurance workflow platforms or IaaS (Insurance as a Service) models help in achieving operational gains in the entire insurance value chain.

AVs are going to dominate the world’s highway because of improved safety and convenience. Companies can leverage this opportunity to introduce innovative autonomous vehicle insurance products.

Growing IoT is blurring the fine-line between different verticals of insurance. To stay competitive, insurers should also indulge in creating new distribution channels and partnerships with OEMs and technology service providers.

Knowledge thats worth delivered in your inbox

Smart Manufacturing starts with real-time visibility.

Manufacturing companies today generate data by the second through sensors, machines, ERP systems, and MES platforms. But without real-time insights, even the most advanced production lines are essentially flying blind.

Manufacturers are implementing real-time dashboards that serve as control towers for their daily operations, enabling them to shift from reactive to proactive decision-making. These tools are essential to the evolution of Smart Manufacturing, where connected systems, automation, and intelligent analytics come together to drive measurable impact.

Data is available, but what’s missing is timely action.

For many plant leaders and COOs, one challenge persists: operational data is dispersed throughout systems, delayed, or hidden in spreadsheets. And this delay turns into a liability.

Real-time dashboards help uncover critical answers:

By converting raw inputs into real-time manufacturing analytics, dashboards make operational intelligence accessible to operators, supervisors, and leadership alike, enabling teams to anticipate problems rather than react to them.

Line performance and downtime trends

Track OEE in real time and identify underperforming lines.

Predictive maintenance alerts

Utilize historical and sensor data to identify potential part failures in advance.

Inventory heat maps & reorder thresholds

Anticipate stockouts or overstocks based on dynamic reorder points.

Quality metrics linked to operator actions

Isolate shifts or procedures correlated with spikes in defects or rework.

These insights allow production teams to drive day-to-day operations in line with Smart Manufacturing principles.

Role-based dashboards

Dashboards can be configured for machine operators, shift supervisors, and plant managers, each with a tailored view of KPIs.

Embedded alerts and nudges

Real-time prompts, like “Line 4 below efficiency threshold for 15+ minutes,” reduce response times and minimize disruptions.

Cross-functional drill-downs

Teams can identify root causes more quickly because users can move from plant-wide overviews to detailed machine-level data in seconds.

Data lakehouse integration

Unified access to ERP, MES, IoT sensor, and QA systems—ensuring reliable and timely manufacturing analytics.

ETL pipelines

Real-time data ingestion from high-frequency sources with minimal latency.

Visualization tools

Custom builds using Power BI, or customized solutions designed for frontline usability and operational impact.

Mantra Labs partnered with a North American die-casting manufacturer to unify its operational data into a real-time dashboard. Fragmented data, manual reporting, delayed pricing decisions, and inconsistent data quality hindered operational efficiency and strategic decision-making.

As this case shows, real-time dashboards are not just operational tools—they’re strategic enablers.

(Learn More: Powering the Future of Metal Manufacturing with Data Engineering)

| Aspect | What You Should Know |

| 1. Why Static Reports Fall Short | Delayed insights after issues occur Disconnected systems (ERP, MES, sensors) No real-time alerts or embedded decision logic |

| 2. What Real-Time Dashboards Enable | Track OEE and downtime in real-time Predictive maintenance using sensor data Dynamic inventory heat maps Quality linked to operators |

| 3. Dashboards That Drive Action | Role-based views (operator to CEO) Embedded alerts like “Line 4 down for 15+ mins” Drilldowns from plant-level to machine-level |

| 4. What Powers These Dashboards | Unified Data Lakehouse (ERP + IoT + MES) Real-time ETL pipelines Power BI or custom dashboards built for frontline usability |

Smart Manufacturing dashboards aren’t just analytics tools—they’re productivity engines. Dashboards that deliver real-time insight empower frontline teams to make faster, better decisions—whether it’s adjusting production schedules, triggering preventive maintenance, or responding to inventory fluctuations.

Explore how Mantra Labs can help you unlock operations intelligence that’s actually usable.

Knowledge thats worth delivered in your inbox

Our Sales Team will be in touch with you shortly.

Hello Stranger! Please fill in a few details,and you’ll receive a link to this case study.

We have mailed you this case study.

We have mailed you this case study.

Thanks for subscribing.