6 minutes, 6 seconds read

Published on Nov 7, 2019

Updated on May 10, 2020

Create superior customer experiences to enhance competitive advantage.

Go from zero to breakthrough with scalable, future-proof solutions.

Harness deep tech for smarter solutions and maximum impact.

Accelerate value delivery with powerful pre-built digital tools.

Help businesses connect with an internet first generation.

Test the smarter way: where precision meets efficiency.

Unlock real-time and personalized customer journeys for mobile first generation.

Turn data into decisive action with scalable AI infrastructure.

Design agile digital foundations that scale with tomorrow's business needs.

Build new-age architecture for maximum efficiency and hyper-growth.

Fine-tune your cloud infrastructure for peak performance.

Automated compliance and control for global regulations.

All

Customer Experience

Mantra

Application Development

Insurtech

Digital Health

Insurance

Deep-Tech

AgriTech(1)

Augmented Reality(21)

Clean Tech(9)

Customer Journey(17)

Design(45)

Solar Industry(8)

User Experience(68)

Edtech(10)

Events(34)

HR Tech(3)

Interviews(10)

Life@mantra(11)

Logistics(6)

Manufacturing(5)

Strategy(18)

Testing(9)

Android(48)

Backend(32)

Dev Ops(11)

Enterprise Solution(33)

Technology Modernization(9)

Frontend(29)

iOS(43)

Javascript(15)

AI in Insurance(41)

Insurtech(67)

Product Innovation(59)

Solutions(22)

E-health(12)

HealthTech(25)

mHealth(5)

Telehealth Care(4)

Telemedicine(5)

Artificial Intelligence(154)

Bitcoin(8)

Blockchain(19)

Cognitive Computing(8)

Computer Vision(8)

Data Science(24)

FinTech(51)

Banking(7)

Intelligent Automation(27)

Machine Learning(48)

Natural Language Processing(14)

The insurance market dynamics are changing rapidly. While a connected ecosystem is the need of the time, agility and new business models are a way through. The current edition of the World InsurTech Report (WITR) emphasizes on developing synergies between Insurers and InsurTechs for the success of the future insurance marketplace. Here are 10 key takeaways from WITR 2019.

Tech giants like Alibaba, Amazon, Apple, Facebook, and Google are entering the Insurance space with enormous customer data. Moreover, customers (nearly 30%) are responding positively to buying insurance products from BigTech firms, according to the World Insurance Report 2018. WITR proposes the following business process improvement for Insurers to remain market-fit.

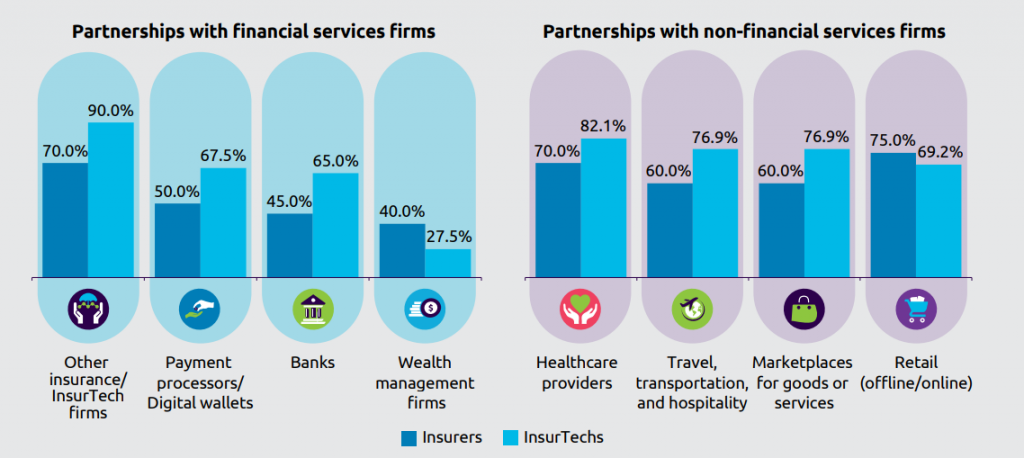

#1 Partnerships with Insurtechs, Financial Institutions and Industry Players

90% of InsurTechs and 70% of Incumbents believe partnerships are crucial. And these partnerships are not confined only to the insurance sector. These can include collaboration with financial, technology, healthcare, travel, transportation, hospitality, retail, and more.

Baloise Insurance partnered with Swiss bank BLKB, and Swiss online insurance broker Anivo to develop a flexible and scalable digital insurance platform with B2C integration. The product released as Bancassurance 2.0 achieved a hit ratio of 50% for video-chat advisory sessions; more than 90% of customers rated the experience as good or very good.

Partnerships can also bring compound insurance products, which otherwise seems impossible. For example, Swiss Re and French cybersecurity InsurTech firm OZON together, launched CyberSolution 360°. It is a risk management solution combining insurance and cyber-attack protection services for small and medium-sized enterprises.

#2 Adopting New Business Models

Not only Insurers, but also customers approve of new insurance models. For instance, 41% of customers are ready to consider usage-based insurance and 37% are willing to explore on-demand coverage. To meet the coverage gaps, offer convenience and personalization, Insurers are adopting the following new business models.

#3 Aligning Strategies with the Future Insurance Marketplace

An insurance marketplace is a viable solution to support a broad spectrum of customer demands. It can also offer coverage for emerging risks and can deliver easy-access compound offerings from individual players of the insurance, manufacturing, and technology ecosystem.

For example, Friday, a Berlin-based startup, launched in 2017, offers digital automotive insurance with kilometre-based billing, flexible tenure, and paperless administration. With telematics support from BMW CarData, Automotive services from ATU, car-rental marketplace Drivy, and distribution channel from Friendsurance, Friday offers customer-centric insurance products.

“The insurance marketplace of the future will provide data and insights about customers that the industry never had before. This will allow firms to design a product closer to customers’ needs and, more importantly, offer them the product when they need it!”

Stephen Barnham, Asia CIO, MetLife

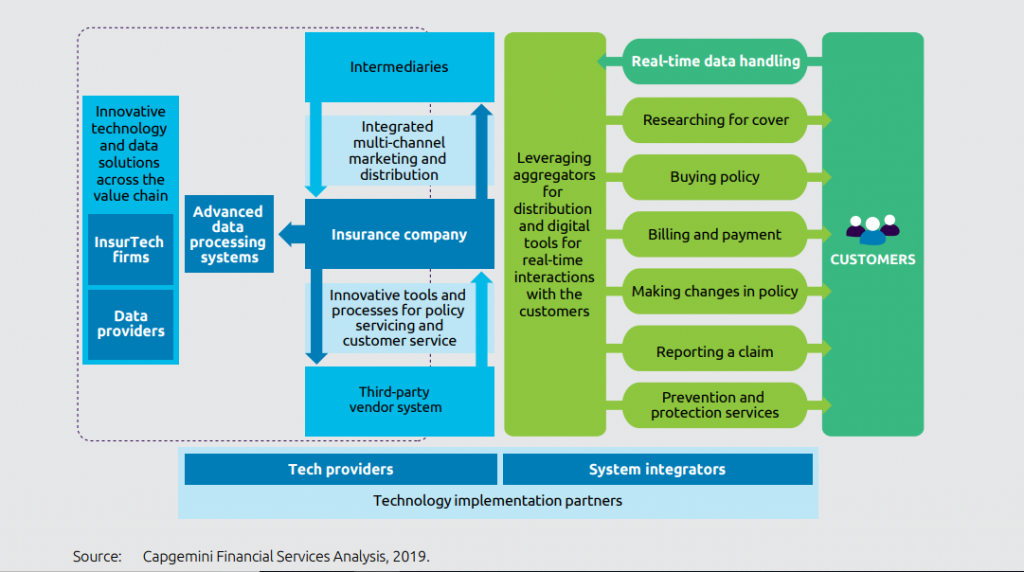

#4 Building an Integrated Ecosystem

As aggregators, OEMs (Original Equipment Manufacturers), policy management apps, and third parties enter the insurance value chain, an integrated insurance ecosystem can smoothen the overall functioning.

For instance, digital integration with aggregators and third parties can broaden the Insurers’ distribution channel. Partnering with OEMs can help them with real-time customer data. Further, APIs, cloud-based storage, and blockchain can foster the insurance ecosystem with data security and transparency.

#5 Being an Inventive Insurer

Inventive Insurers are the ones who have strategically updated their product portfolios, operating models, and distribution methods. They are realistic about their competencies. By identifying their distinct capabilities and partnering with other players to bridge their competency gap, Inventive Insurers can deliver an end-to-end product to the customers.

The World InsurTech Report 2019 defines the competencies of Inventive Insurers as follows –

The tech-savvy customers are seeking easy-to-understand products with the facility of direct online purchases. Even leading Insurer like Berkshire Hathaway’s Insurance Group – BiBerk launched ‘THREE’ – only three pages long product covering workers’ compensation, liability, property, and auto to catch the pace. The drift is towards the following new insurance products.

#6 Bundling Financial and Non-financial offerings

An insurance package comprising both financial and non-financial products can expand an Insurer’s products portfolio, giving a competitive edge. It can also help in pitching new prospects. Bundling products and services will increase customer touchpoints and can help insurers identify their needs more effectively.

For example, Homeflix insurance provides renters and homeowners insurance to its core. In addition to insurance coverage, it also offers concierge maintenance services like plumbing and electricity. The company also plans home delivery, babysitting, and cleaning services next.

#7 Tailored Products

Traditional insurance policies don’t fit today’s desire for add-on services, personalization, and flexible offerings. The World Insurance Report 2019 survey found that more than 75% of B2B customers and 85% of retail policyholders believe they’re not covered against the emerging risks.

Being aware of the need for customized products, 84% of Insurers and 80% of InsurTechs say they are focusing on “developing new offerings.”

#8 Products that Engage and Educate Customers

Gamification, video-chat sessions, and social media are promising channels for engaging with customers and educating them about risks and their need for coverage. Healthy interactions with customers through their preferred channels can boost sales.

“Insurers should focus on providing user friendly, transparent information via digital channels, allowing customers to make an informed decision. This will be critical not only for upselling, but also for attracting more new-generation customers, who are tech savvy and want to make faster product decisions.”

Jas Maggu, CEO, Galaxy.AI

For operational success- understanding customer preferences, conceptualizing new products portfolio, partnerships, and an effective go-to-market strategy is crucial. Fundamental shifts in the current operational models towards experience-driven solutions, strategic use of data, partnerships, and shared ownership of assets portray emerging trends.

#9 Embracing Digital Agility

70% of insurers and 85% of InsurTechs believe a lack of technological readiness is a critical concern.

The more quickly Insurers implement initiatives, the closer they will be to achieve the digital maturity and hence actively participate in the connected ecosystem. The agile digital infrastructure demands real-time data gathering and analytics and automation of complex processes.

It will also lead to product agility. Insurers can offer new products at a faster pace and with reduced GTM (go-to-market) time, they can gain a competitive advantage.

Join our Webinar — AI for Data-driven Insurers: Challenges, Opportunities & the Way Forward hosted by our CEO, Parag Sharma as he addresses Insurance business leaders and decision-makers on April 14, 2020.

#10 Automating Processes

Not only claims processing and underwriting, but much more insurance back and front-office operations can also be automated. Automation brings two-fold benefit to the insurers. One- mundane tasks are carried by machines, speeding the processes and freeing humans for sophisticated work. The other benefit lies in enhanced accuracy.

For example, AIA Hongkong has improved claims processing time by 40% through AI-driven ICR techniques and intelligent process automation.

Read claims automation case study: How AIA Hong Kong saves 60% through claims automation.

Deutsche Familienversicherung (DFV) provides a digital automated platform for property and supplementary health insurance. It can process the transactions in real-time enabling customers to file claims and receive feedback immediately. Moreover, policyholders can engage with the firm via several digital channels, including Amazon Alexa.

Source: World InsurTech Report 2019

We’re AI-first products and solutions firm for the new-age digital insurer recognized among the InsurTech100 for pioneering the transformation of the global insurance industry. Drop us a line at hello@mantralabsglobal.com to know more about our offerings.

Knowledge thats worth delivered in your inbox

Smart Manufacturing starts with real-time visibility.

Manufacturing companies today generate data by the second through sensors, machines, ERP systems, and MES platforms. But without real-time insights, even the most advanced production lines are essentially flying blind.

Manufacturers are implementing real-time dashboards that serve as control towers for their daily operations, enabling them to shift from reactive to proactive decision-making. These tools are essential to the evolution of Smart Manufacturing, where connected systems, automation, and intelligent analytics come together to drive measurable impact.

Data is available, but what’s missing is timely action.

For many plant leaders and COOs, one challenge persists: operational data is dispersed throughout systems, delayed, or hidden in spreadsheets. And this delay turns into a liability.

Real-time dashboards help uncover critical answers:

By converting raw inputs into real-time manufacturing analytics, dashboards make operational intelligence accessible to operators, supervisors, and leadership alike, enabling teams to anticipate problems rather than react to them.

Line performance and downtime trends

Track OEE in real time and identify underperforming lines.

Predictive maintenance alerts

Utilize historical and sensor data to identify potential part failures in advance.

Inventory heat maps & reorder thresholds

Anticipate stockouts or overstocks based on dynamic reorder points.

Quality metrics linked to operator actions

Isolate shifts or procedures correlated with spikes in defects or rework.

These insights allow production teams to drive day-to-day operations in line with Smart Manufacturing principles.

Role-based dashboards

Dashboards can be configured for machine operators, shift supervisors, and plant managers, each with a tailored view of KPIs.

Embedded alerts and nudges

Real-time prompts, like “Line 4 below efficiency threshold for 15+ minutes,” reduce response times and minimize disruptions.

Cross-functional drill-downs

Teams can identify root causes more quickly because users can move from plant-wide overviews to detailed machine-level data in seconds.

Data lakehouse integration

Unified access to ERP, MES, IoT sensor, and QA systems—ensuring reliable and timely manufacturing analytics.

ETL pipelines

Real-time data ingestion from high-frequency sources with minimal latency.

Visualization tools

Custom builds using Power BI, or customized solutions designed for frontline usability and operational impact.

Mantra Labs partnered with a North American die-casting manufacturer to unify its operational data into a real-time dashboard. Fragmented data, manual reporting, delayed pricing decisions, and inconsistent data quality hindered operational efficiency and strategic decision-making.

As this case shows, real-time dashboards are not just operational tools—they’re strategic enablers.

(Learn More: Powering the Future of Metal Manufacturing with Data Engineering)

| Aspect | What You Should Know |

| 1. Why Static Reports Fall Short | Delayed insights after issues occur Disconnected systems (ERP, MES, sensors) No real-time alerts or embedded decision logic |

| 2. What Real-Time Dashboards Enable | Track OEE and downtime in real-time Predictive maintenance using sensor data Dynamic inventory heat maps Quality linked to operators |

| 3. Dashboards That Drive Action | Role-based views (operator to CEO) Embedded alerts like “Line 4 down for 15+ mins” Drilldowns from plant-level to machine-level |

| 4. What Powers These Dashboards | Unified Data Lakehouse (ERP + IoT + MES) Real-time ETL pipelines Power BI or custom dashboards built for frontline usability |

Smart Manufacturing dashboards aren’t just analytics tools—they’re productivity engines. Dashboards that deliver real-time insight empower frontline teams to make faster, better decisions—whether it’s adjusting production schedules, triggering preventive maintenance, or responding to inventory fluctuations.

Explore how Mantra Labs can help you unlock operations intelligence that’s actually usable.

Knowledge thats worth delivered in your inbox

Our Sales Team will be in touch with you shortly.

Hello Stranger! Please fill in a few details,and you’ll receive a link to this case study.

We have mailed you this case study.

We have mailed you this case study.

Thanks for subscribing.