3 minutes, 56 second read

Published on Jan 8, 2020

Updated on May 11, 2020

Create superior customer experiences to enhance competitive advantage.

Go from zero to breakthrough with scalable, future-proof solutions.

Harness deep tech for smarter solutions and maximum impact.

Accelerate value delivery with powerful pre-built digital tools.

Help businesses connect with an internet first generation.

Test the smarter way: where precision meets efficiency.

Unlock real-time and personalized customer journeys for mobile first generation.

Turn data into decisive action with scalable AI infrastructure.

Design agile digital foundations that scale with tomorrow's business needs.

Build new-age architecture for maximum efficiency and hyper-growth.

Fine-tune your cloud infrastructure for peak performance.

Automated compliance and control for global regulations.

All

Customer Experience

Mantra

Application Development

Insurtech

Digital Health

Insurance

Deep-Tech

AgriTech(1)

Augmented Reality(21)

Clean Tech(9)

Customer Journey(17)

Design(45)

Solar Industry(8)

User Experience(68)

Edtech(10)

Events(34)

HR Tech(3)

Interviews(10)

Life@mantra(11)

Logistics(6)

Manufacturing(5)

Strategy(18)

Testing(9)

Android(48)

Backend(32)

Dev Ops(11)

Enterprise Solution(33)

Technology Modernization(9)

Frontend(29)

iOS(43)

Javascript(15)

AI in Insurance(41)

Insurtech(67)

Product Innovation(59)

Solutions(22)

E-health(12)

HealthTech(25)

mHealth(5)

Telehealth Care(4)

Telemedicine(5)

Artificial Intelligence(154)

Bitcoin(8)

Blockchain(19)

Cognitive Computing(8)

Computer Vision(8)

Data Science(24)

FinTech(51)

Banking(7)

Intelligent Automation(27)

Machine Learning(48)

Natural Language Processing(14)

Human Behavior is inherently hard to predict and mostly irrational. Infact, this irrationality is often overlooked because it offers no meaningful insight or patterns behind our motivations.

In the early 70’s, Israeli-American economist Daniel Kahneman challenged the assumption that humans behave rationally when making financial choices. His research explored the fundamentals of how people handle risk and display bias in economic decision-making. He would later be awarded the Nobel Prize for his pioneering work which provided the basis for an entirely new field of study called Behavioral Economics.

Standard Economics assumes humans behave rationally, whereas Behavioral economics factors in human irrationality in the buying process.

Along with another scientific approach to studying natural human behaviors (Behavioral Science), both these fields became particularly useful to the financial industry early on. By understanding the deep seated motivations behind people’s choices, a specific interaction can be designed to influence an individual’s behavior — also known as behavioral intervention.

By finding meaningful patterns in Big Data, usually performed by a data scientist, businesses are able to leverage analytics and behavioral customer psychology. The outcomes of these insights can help business owners learn about the customer’s true feeling, explore behavioral pricing strategies, design new experiences and retain more loyal buyers. This is why Behavioral Scientists have become highly sought after over the last decade.

Take for instance Dan Ariely, who is a Professor of Psychology & Behavioral Economics at Duke University, and also serves as the Chief Behavioral Officer of Lemonade — the World’s biggest Insurtech. Ariely observes that human behavior is ‘predictably irrational’ and constantly exhibits ‘self-defeating’ characteristics. There is a lot of value in studying these behaviors, for many organizations, to encourage positive ones, dissuade dishonesty and improve the underlying relationship.

The ‘dissuading dishonesty’ part is particularly useful for Insurance carriers. For a business that fundamentally deals with both people and risk, Insurance is endlessly plagued by fraud. Insurance fraud losses were estimated around $80B in 2019 alone. On the other hand, legitimate claim instances can at times be overlooked due to the lack of evidence or nuances in the finer policy details.

To combat fraud during the claims process, Ariely added a simple ‘honesty pledge’ agreement before the beginning of the claims intimation process. A customer signs the digital pledge, and is then asked to record a short video explaining the incident for which they are requesting the claim.

The process seems naive but it’s backed by tons of data and science — a byproduct of decades of research work put into psychology and behavioral economics.

So, How are claims being driven by data science?

How do insurers capture honesty from their customers?

The answer is priming.

By enforcing an honesty pledge, Lemonade was able to bring down the likelihood of fraudulent claims being intimated for. In other words, they made it harder for customers to lie. The hypothesis that works is: Don’t blame people for mistakes in decision making, it’s on the designers of the system.

After the customer got done with their video recording, Lemonade ran 18 anti-fraud algorithms against the claim to check its veracity and a payment was made in a few seconds.

Behavioral work is built on strong academic research that identifies aspects that influence the buying process. ‘Nudges’ are a perfect example of behavioral priming at work. Nudge theory (a concept within Behavioral Science) identifies positive reinforcement techniques as ways to influence a person’s behavior and ultimately their decision-making.

For example, according to a study published in the Journal of Marketing Research, research subjects who were shown an aged image of their faces allocated twice the amount to their retirement savings when compared to people who were shown images of their current younger selves.

In this case, the ‘nudging’ technique was effective in driving retirement planning behavior among the test group.

Source: Centre for Financial Inclusion

Behavioral Economics also stipulates that once you start doing something, you are more likely to continue doing so. This is how Netflix uses subtle nudges on their platform, where after each episode a prompt asks if you would like to continue watching the show.

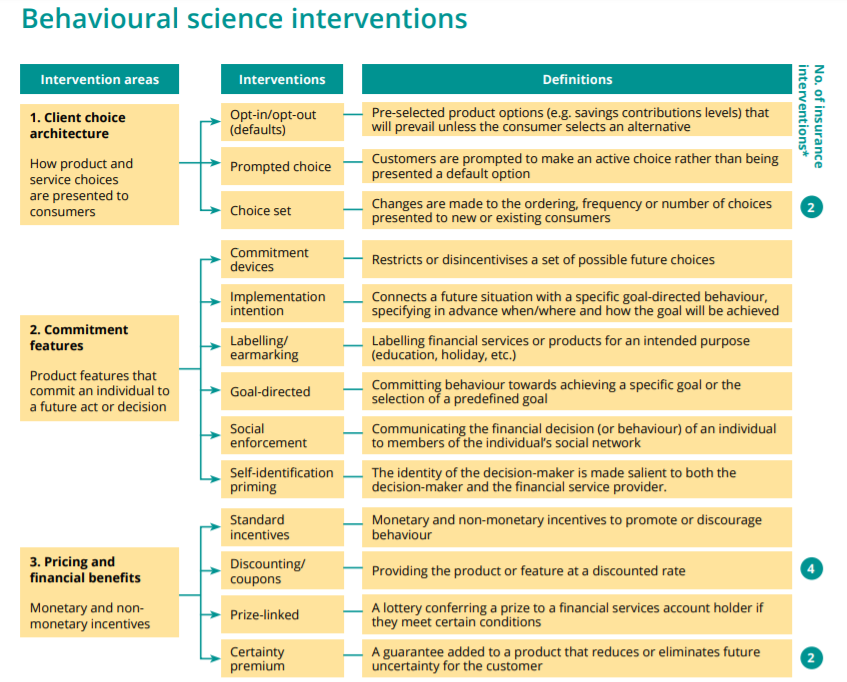

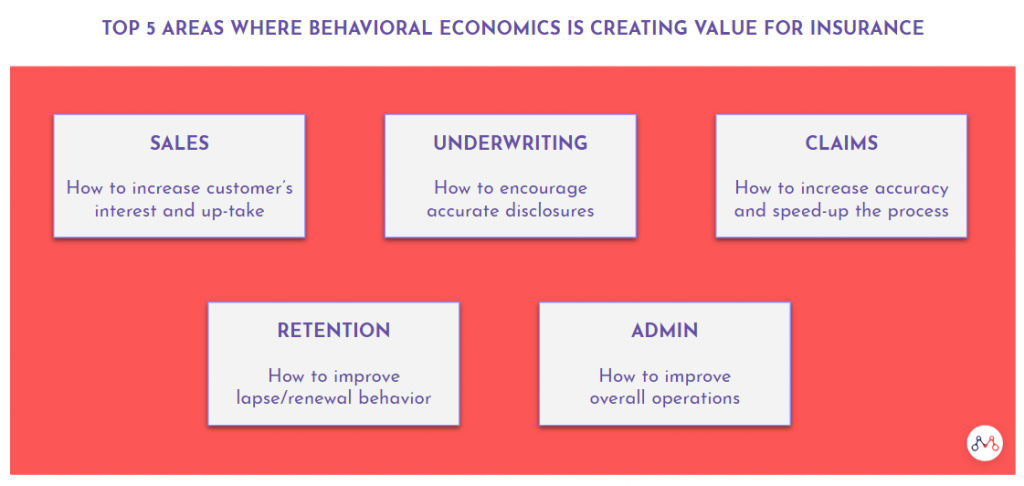

Swiss Re’s Behavioural Research Unit outlines five promising areas where behavioral economics can create new value for insurers.

Digital businesses are gradually realizing the limitations of human and machine systems without any real intelligence or computing power behind it. Between human prone errors and the scalability challenges of traditional technologies, a new mechanism is required to learn and adapt better.

Behavioral Science interventions in insurance can help carriers align their strategies with the true needs of their customers. Using the insights posited from advanced machine learning models, the right behavioral intervention can bring about changes to real-world insurance demand behavior that closely matches the benchmark model.

Also read – how InsurTech beyond 2020 will be different?

Knowledge thats worth delivered in your inbox

Smart Manufacturing starts with real-time visibility.

Manufacturing companies today generate data by the second through sensors, machines, ERP systems, and MES platforms. But without real-time insights, even the most advanced production lines are essentially flying blind.

Manufacturers are implementing real-time dashboards that serve as control towers for their daily operations, enabling them to shift from reactive to proactive decision-making. These tools are essential to the evolution of Smart Manufacturing, where connected systems, automation, and intelligent analytics come together to drive measurable impact.

Data is available, but what’s missing is timely action.

For many plant leaders and COOs, one challenge persists: operational data is dispersed throughout systems, delayed, or hidden in spreadsheets. And this delay turns into a liability.

Real-time dashboards help uncover critical answers:

By converting raw inputs into real-time manufacturing analytics, dashboards make operational intelligence accessible to operators, supervisors, and leadership alike, enabling teams to anticipate problems rather than react to them.

Line performance and downtime trends

Track OEE in real time and identify underperforming lines.

Predictive maintenance alerts

Utilize historical and sensor data to identify potential part failures in advance.

Inventory heat maps & reorder thresholds

Anticipate stockouts or overstocks based on dynamic reorder points.

Quality metrics linked to operator actions

Isolate shifts or procedures correlated with spikes in defects or rework.

These insights allow production teams to drive day-to-day operations in line with Smart Manufacturing principles.

Role-based dashboards

Dashboards can be configured for machine operators, shift supervisors, and plant managers, each with a tailored view of KPIs.

Embedded alerts and nudges

Real-time prompts, like “Line 4 below efficiency threshold for 15+ minutes,” reduce response times and minimize disruptions.

Cross-functional drill-downs

Teams can identify root causes more quickly because users can move from plant-wide overviews to detailed machine-level data in seconds.

Data lakehouse integration

Unified access to ERP, MES, IoT sensor, and QA systems—ensuring reliable and timely manufacturing analytics.

ETL pipelines

Real-time data ingestion from high-frequency sources with minimal latency.

Visualization tools

Custom builds using Power BI, or customized solutions designed for frontline usability and operational impact.

Mantra Labs partnered with a North American die-casting manufacturer to unify its operational data into a real-time dashboard. Fragmented data, manual reporting, delayed pricing decisions, and inconsistent data quality hindered operational efficiency and strategic decision-making.

As this case shows, real-time dashboards are not just operational tools—they’re strategic enablers.

(Learn More: Powering the Future of Metal Manufacturing with Data Engineering)

| Aspect | What You Should Know |

| 1. Why Static Reports Fall Short | Delayed insights after issues occur Disconnected systems (ERP, MES, sensors) No real-time alerts or embedded decision logic |

| 2. What Real-Time Dashboards Enable | Track OEE and downtime in real-time Predictive maintenance using sensor data Dynamic inventory heat maps Quality linked to operators |

| 3. Dashboards That Drive Action | Role-based views (operator to CEO) Embedded alerts like “Line 4 down for 15+ mins” Drilldowns from plant-level to machine-level |

| 4. What Powers These Dashboards | Unified Data Lakehouse (ERP + IoT + MES) Real-time ETL pipelines Power BI or custom dashboards built for frontline usability |

Smart Manufacturing dashboards aren’t just analytics tools—they’re productivity engines. Dashboards that deliver real-time insight empower frontline teams to make faster, better decisions—whether it’s adjusting production schedules, triggering preventive maintenance, or responding to inventory fluctuations.

Explore how Mantra Labs can help you unlock operations intelligence that’s actually usable.

Knowledge thats worth delivered in your inbox

Our Sales Team will be in touch with you shortly.

Hello Stranger! Please fill in a few details,and you’ll receive a link to this case study.

We have mailed you this case study.

We have mailed you this case study.

Thanks for subscribing.